Iron Mountain, Outfront Media, and LTC Properties are all high-quality stocks that offer investors income and growth potential.

It is not hard to figure out why so many investors love dividend stocks. Dividend payments allow shareholders to generate an income stream from their stocks without having to sell. That money can be used as spending money or capital that can be reinvested elsewhere.

Of course, just because a company pays a dividend doesn’t make it an automatic buy. In fact, I think investors need to be picky about which dividend stocks they own.

So, which dividend stocks do I think are buys right now? Here’s why I believe Iron Mountain (NYSE:IRM), Outfront Media (NYSE:OUT), and LTC Properties(NYSE:LTC) are all top choices.

A storage giant

Kicking off our list today is Iron Mountain. This company is primarily focused on providing other businesses with data management and storage solutions. Iron Mountain provides this service to more than 220,000 unique customers from around that world, which includes 94% of the Fortune 1000.

What’s wonderful about the storage business is that customers are willing to sign multiyear agreements to help keep their documents safe. Those agreements help to keep revenue flowing into Iron Mountain’s bank account even during economic slowdowns. In addition, maintenance costs on storage facilities tend to be quite low, which helps keeps the company’s expenses under control. When combined, Iron Mountain benefits from a steady profit stream that it uses to fund a growing dividend.

Looking ahead, management has announced a realistic plan to steadily increase its revenue and profits between now and 2020. The plan calls for $100 million in annual spending on acquisitions and the continued build out of its capabilities in art storage and data-center management. When added to modest growth in its core record keeping and document-shredding businesses, management believes single-digit top- and bottom-line growth is achievable. If true, the company should easily be able to afford regular dividend increases in the years ahead. That’s a compelling investing thesis for a company that already boasts a yield of 6.1%.

Advertising you can’t ignore

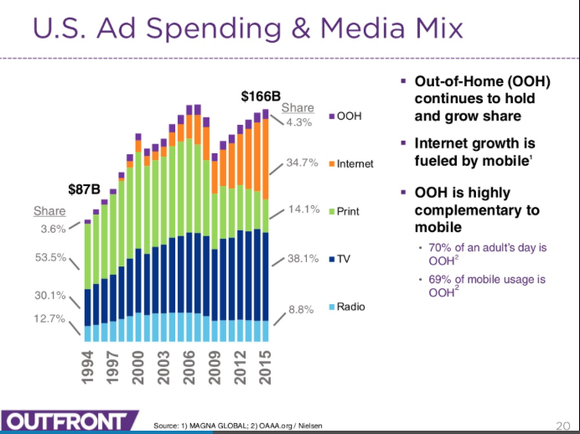

Between ad blockers and DVRs, most consumers will do just about anything to minimize the amount of advertising they see on a given day. However, there’s not much a consumer can do avoid billboards or advertisements on public transportation systems. That why these “out-of-home” advertising methods remain a popular choice for companies who want to market their products or services.

Outfront Media is a leading provider of these out-of-home advertising assets. Say you wanted to place an ad on a billboard, bus, commuter rail, subway, or sports stadium. In that case, Outfront Media is the company you’d want to talk to. Outfront can help you quickly get your message out thanks to its network of 352,000 displays that are strategically placed throughout the country. That’s why top advertisers like Apple, McDonald’s, and Verizon choose to team up with Outfront.

You are likely aware that the advertising landscape has shifted in recent years in favor of online channels like Facebook and Alphabet. However, that spending shift has largely come at the expense of radio and print. In fact, out-of-home advertising has actually modestly grown its overall market share of ad spending over the last two decades.

IMAGE SOURCE: OUTDOOR MEDIA.

Looking forward, Outfront appears to have a solid profit growth plan in place. That plan calls for strategic acquisitions, modest performance improvement, and growth initiatives such as leasing out space on its billboards for use as cell towers. In total, Outfront looks poised to drive modest profit growth over the long term. When adding in the company’s market-topping dividend yield of 5.3%, Outfront looks like a solid dividend stock.

The wind at its back

America’s population is getting older. In fact, by 2030, the population of Americans aged 75 and older is expected to nearly double when compared to 2012. That dramatic demographic shift should ensure that the demand for skilled nursing or assisted-living facilities remains strong for years to come. That’s a wonderful tailwind for a company like LTC properties.

LTC Properties owns more than 200 assisted-living, memory-care, and skilled nursing facilities in 30 U.S. states. What I like about this business is that LTC is just a landlord that outsources all of the day-to-day facilities management to a group of trusted operators. That allows LTC to remain focused on acquiring new buildings.

LTC has been running this simple but effective business model for years. The company has grown considerably over the last few decades and has paid out a healthy dividend for more than 20 straight years. At current prices, the company’s dividend yield is just over 4.6%.

Over the long term, LTC looks poised for growth. That’s because the U.S. healthcare real estate market is highly fragmented and has more than $1 trillion in total assets outstanding. That leaves LTC with plenty of room left to slowly build out its empire and share its growing profits with investors.

Forget Iron Mountain: These are the best dividend stocks to buy now

If you’re looking for solid income from dividend stocks, look no further. The Motley Fool’s top dividend analyst, who leads our dividend stock newsletter, Income Investor, just picked what he believes are the best income stocks in the market right now… and Iron Mountain didn’t make the list!

These dividend cash cows could be the latest in a long string of market-beating stocks Income Investor has picked over the years.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Brian Feroldi owns shares of Alphabet (A and C shares), Apple, and Facebook. The Motley Fool owns shares of and recommends Alphabet (A and C shares), Apple, Facebook, and Verizon Communications. The Motley Fool has a disclosure policy.